Overview

In Q2 2024, the North American consumer and retail sectors demonstrated resilience despite various economic challenges. The quarter presented a mix of challenges and opportunities for retailers, including limited leasing activity and rising operating costs. Notably, US consumer prices fell in June for the first time in four years, driven by cheaper gasoline prices and gradually moderating rents. This shift toward disinflation prompted the Federal Reserve to cut interest rates in September, marking the first interest rates cut since the COVID-19 pandemic.

Contrary to earlier forecasts predicting distress among lower-income households, the economic landscape has remained robust, supported by increase in wages and sustained job growth. While overall financial well-being remains stable, positive trends among higher-income households may overshadow emerging weaknesses among average earners. Consumer sentiment in the US experienced a slight decline, with the University of Michigan’s index dropping from 68.2 in June to 66.4 in July, reflecting ongoing concerns about high prices, especially among lower-income households. Meanwhile, inflation expectations for the year ahead decreased to 2.9%, and long-term expectations remained steady at 3.0%. Although the labor market continues to bolster consumer spending, uncertainty around the upcoming election has added volatility to the economic outlook.

Retail and food service sales in the US grew by 2.7% Y-o-Y to $2,111.5 billion in Q2 2024, up from $2,056.9 billion in Q2 2023, according to seasonally adjusted data from the US Census Bureau. The upside can be attributed to segments like clothing and accessories, general merchandise, food and beverage, and electronics and appliances. Consumer spending, which accounts for over two-thirds of the US economy, rose by 2.3%, boosted by higher expenditure on services such as healthcare, housing, recreation, and gambling, as well as goods like new vehicles, furnishings, and energy products.

However, US retail sales remained flat M-o-M in June at $704.3 billion, with a decline in auto dealership receipts balanced by gains in other segments. In contrast, Canadian retail and food services sales fell by 0.8% MoM to C$66.1 billion in May, as reported by Statistics Canada. Preliminary estimates suggested a continued decline in June, indicating cautious consumer behavior amid high interest rates.

Figure 1: Y-o-Y Change (%) in US Retail Sales

According to the US Bureau of Labor Statistics, the labor market showed signs of weakening amid a hiring slowdown and potential recession risks. The unemployment rate rose to 4.3% in July, up from 4.1% in June, with the number of unemployed individuals increasing by 352,000 to 7.2 million. Despite the overall deterioration, certain sectors, including healthcare, construction, and leisure and hospitality, experienced job growth. The retail sector saw a modest addition of 4,000 jobs, mainly in general merchandise and automobile dealerships.

M&A Activity

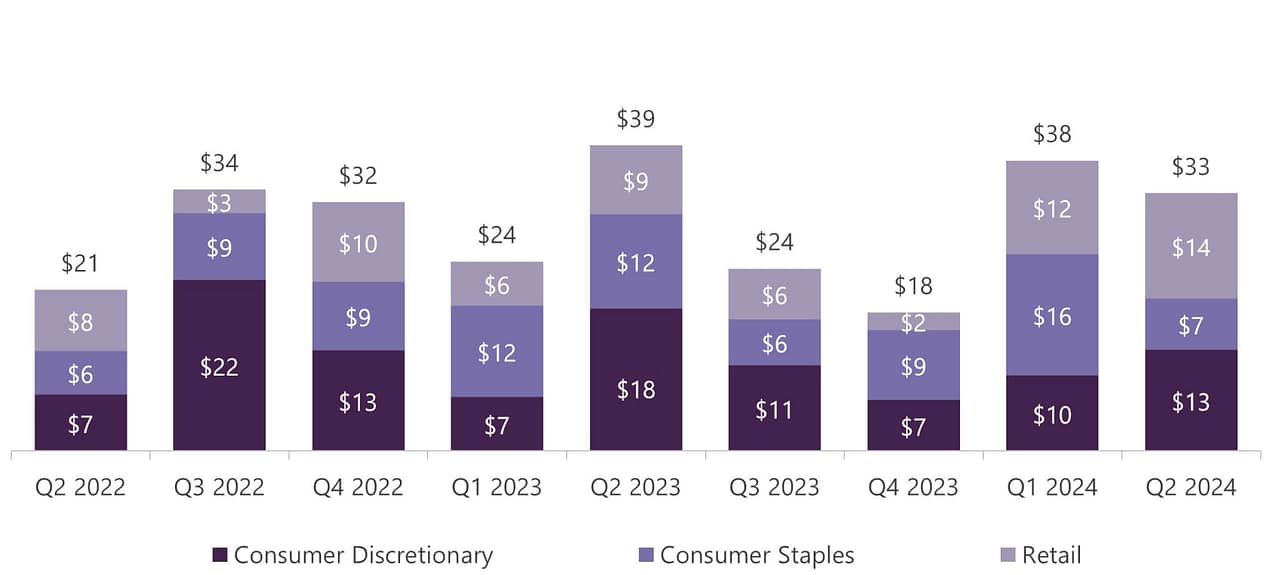

M&A activity in the consumer and retail sectors across the Americas (North America, the Caribbean, and Latin America) remained weak. It declined by 53.1% to $13.9 billion in Q2 2024, from $29.5 billion in Q1 2024. This significant downturn was driven by a notable drop in M&A activity across three segments, as dealmaking continued to struggle due to persistent macroeconomic and geopolitical challenges.

The financing environment for M&A and leveraged buyouts (LBOs) remained particularly difficult. Central banks across the Americas have kept interest rates high, making financing more costly for both strategic acquirers and financial sponsors. This high-interest rate environment has tightened access to capital, further dampening the prospects for dealmaking.

Given the ongoing global economic struggles, we anticipate that M&A activity in the consumer and retail sectors will likely remain subdued through the end of 2024.

Figure 2: M&A Deal Value

(USD billion)

Bankruptcies

The retail sector’s challenges have become increasingly evident with a noticeable rise in insolvencies in H1 2024. As of July 16, 21 retailers in the US had filed for bankruptcy, marking the highest number recorded during this period since 2020.

The surge in bankruptcies is primarily driven by rising debt burdens due to high interest rates and inflation, along with stricter lending standards. These factors have strained retailers’ finances, pushing many towards insolvency. We expect this trend to continue with more retailers seeking bankruptcy protection in the coming months.

Figure 3: Number of Bankruptcies in US Retail Sector (2010 – YTD 2024)

*Due to a change in the Global Industry Classification Standard in March 2023, as well as a methodology change to exclude distributors, results starting with the April 2023 publication will not match prior publications.

Capital Market Activity

Debt-raising activities in the Americas declined by 5.2% to $46.8 billion in Q2 2024, compared with $49.3 billion in Q1 2024. The downside can be attributed to a slowdown in debt-raising activities within the consumer discretionary and consumer staples segments. The prevailing high interest rate environment has significantly slowed both LBOs and the broader M&A market. Despite this, refinancing and repricing activities continued to dominate the high-yield bond and leveraged loan markets as issuers renegotiated existing loans to secure lower margins amid improving market conditions.

With the Federal Reserve concluding its tightening cycle in September, we expect a resurgence in M&A and LBO activities. The Fed's recent half-point rate cut signals easing financial conditions. As borrowing costs decrease, both borrowers and lenders will likely benefit from a more favorable financing environment, supporting a rebound in deal activity as market conditions improve.

Figure 4: DCM Quarterly Deal Volume

(USD billion)

Equity-raising activities in the Americas declined by 11.3% to $33.3 billion in Q2 2024, down from $37.5 billion in Q1 2024. The decrease was primarily driven by a notable dip in equity-raising activities within the consumer staples segment. During Q2 2024, there was a slowdown in IPO activity, primarily due to high inflation, rising interest rates, and overall economic uncertainty.

We anticipate a potential increase in IPOs early next year, provided that returns remain favorable and market conditions show signs of improvement.

Figure 5: ECM Quarterly Deal Value

(USD billion)

The Road Ahead

A slowdown in inflation is expected to support retail volume growth but depleted savings and high food prices may temper its progress. Retail sales in the US are projected to rise by 6.7% in dollar terms and 2.0% in volume terms in 2024, aided by moderating inflation. However, with households having drawn down much of their savings, consumers’ price sensitivity will remain high.

Despite economic challenges, e-commerce activities in the US are set to grow and take up a larger share of the retail market this year. Sales are expected to reach $1.2 trillion by the end of the year. The retail sector is adapting by turning stores into fulfillment centers, closing underperforming locations, using AI, and blending online and offline shopping experiences. This shift highlights the growing importance of integrating online and physical retail strategies.

Elevated trade tensions between the US and China, the Russia-Ukraine conflict, and instability in the Middle East are expected to add to the uncertainties and risks heading into the latter half of 2024. While direct economic impacts in the US have been limited so far, a potential supply shock in critical commodities such as energy, food, or semiconductors could significantly disrupt markets. Additionally, the US presidential election may influence geopolitics more than in recent cycles, given the current tensions.

The pressure on companies to transform through M&A to meet evolving consumer needs remains high. We expect dealmakers to focus on transformation and readiness, with M&A activity likely to gain momentum over the next 6 to 12 months as market conditions stabilize.

Capital market activities in the consumer sector are expected to improve in H2 2024 after a challenging period. The outlook for debt markets remains positive, with issuers successfully extending maturities and investor demand for risk assets holding steady. As inflation eases and interest rates decline further, M&A and LBO pipelines could see a resurgence in activities.

Overall, the North American consumer and retail sectors are poised to navigate a complex landscape shaped by economic indicators, market activities, and geopolitical events. To excel in these sectors, companies must stay updated about employment trends, debt markets, and global geopolitical developments. They should also focus on strategic decision-making, as it will be essential to navigate the opportunities and challenges over the coming months.

About Evalueserve

Evalueserve is a leading analytics partner to Fortune 500 companies. Powered by mind+machine™, the company combines insights drawn from data and research with the efficiency of digital tools and platforms to design impactful solutions. Its global team of 4,000+ experts collaborates with clients across 15+ industries.

Connect with us on LinkedIn

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.