As we move through 2024, several notable trends are shaping the landscape of commercial and corporate lending in Europe. Following a period of tight credit conditions and declining loan demand, signs of recovery are emerging as economic outlooks improve and interest rates are adjusted. European banks are leveraging digital transformation, incorporating AI and cloud technologies to enhance efficiency and customer experience. Outsourcing is playing a pivotal role in speeding up these advancements.

Below, we dive into the key factors influencing lending practices in Europe:

1. Turnaround of tightening credit conditions and declining loan demand

Enterprise lending in the eurozone has been marked by tightening credit standards throughout 2023 and the first quarter of 2024. In particular, banks are more stringent about credit terms, often requiring more collateral and imposing higher interest rates to mitigate perceived risks. However, this trend is steadily subsiding, with recent readings showing slighter tightening. The dynamic is similar for loans to SMEs and large corporates and is driven by banks’ heightened risk perceptions due to concerns over the economic outlook and credit risk for firms related to their financial situation.

Since 2022, European banks have also been facing a declining demand for enterprise loans, particularly due to high interest rates and the contraction in companies' capital expenditures. However, the outlook has been steadily improving since mid-2023, and the net decrease in loan demand is expected to become even less pronounced for the remainder of the year.

Source: ECB

As inflation is expected to continue easing during 2024, central banks will fine-tune their monetary policies throughout the year, leading to lower interest rates and, subsequently, a revival in loan demand. The ECB already cut its key interest rate in June by a quarter point, from 4% to 3.75%, moving ahead of the U.S. Fed and signaling a long-awaited change in monetary policy.

2. Digital transformation and AI adoption to retain and gain market share

Globally, banks are increasingly integrating digital technologies into their lending processes. This adoption includes innovations in loan origination, B2B payments, trade finance, and cash management. This digital transformation aims to enhance customer experience, streamline operations, and manage costs effectively. AI and blockchain are being employed to expedite loan approvals, reduce fraud, and improve transparency.

With Big Tech players and smaller fintechs capturing market share from incumbents over the past decade, plus COVID-19 accelerating the transition to online banking, adapting to this dynamic environment was crucial for European banks.

Most of the region’s banks only started developing their digital transformation strategy in recent years, targeting revenue and cost objectives. According to the ECB's 2023 survey on digital transformation, 43% of banks' top five projects are aimed at revenue/customer experience enhancement, and 83% of banks see process automation as a means to reduce costs.

Almost every bank in the Single Supervisory Mechanism has a digital transformation strategy in place and a coordination body to steer the design and implementation of this strategy. They have, on average, allocated 2.8% of their operating income and +5% of their workforce to digital transformation projects (according to the latest ECB survey based on 2021 data).

European banks extensively use APIs and cloud computing, which they see as the foundation of digital transformation. However, 60% of banks under ECB supervision have also reported using AI to facilitate online customer transactions, streamline processes, and provide automated suggestions to customers based on their preferences.

Source: ECB

While AI is commonly perceived to have lower business relevance, some see it as a game changer in the banking industry, especially in commercial banking. Some consultants are discussing potential double-digit improvement in banks' operating income by leveraging generative AI across all commercial banking processes and roles. Some key areas where generative AI can bring significant value in commercial banking are client onboarding, generation of credit memos, and loan servicing.

3. Rise in outsourcing

To accelerate digitalization, European banks turned to external partnerships and outsourcing, the latter being regarded as a catalyst for digital transformation through access to innovation and the latest technology. According to ECB data for 2023, 73 out of +100 significant institutions overseen by the watchdog are currently using critical services provided by non-EU countries under a EUR 25bn allocated budget.

On average, banks' number of contracts with external providers for critical functions have grown by 21%, from 81 in 2022 to 98 in 2023. The number of external providers of critical functions per bank also increased on average by 16%, from 49 in 2022 to 57 in 2023.

A need for standardization combined with digitization is expected to further drive the use and the variety of outsourcing.

Source: ECB

4. Push towards sustainable lending

Alongside digitalization, there’s a strong push in Europe towards green finance. Sustainability-linked loans and ESG financing are on the rise, driven by regulatory pressures and market demand. Environmental Finance said the volume of sustainable loans exceeded USD 860bn in 2023, with more than 80% in a sustainability-linked format. This trend reflects a commitment within the European banking sector to support environmentally sustainable projects and businesses, partly driven by European Sustainability Reporting Standards (ESRS), which officially entered into force on January 1st, 2024 (yet reporting is planned for 2025).

ESRS is a set of rules defining how large EU and non-EU companies with a significant presence in Europe’s economy report on their sustainability performance. They will require them to provide more detailed, granular data about their business’s impact on sustainability. The effect of ESRS on European commercial and corporate banking is expected to be profound, driving significant changes in risk management, credit assessment, investment strategies, product development, transparency, competitiveness, and regulatory compliance. Banks successfully integrating these standards will be better positioned to manage risk and contribute to sustainable economic growth.

It is worth noting that European banks are also incorporating ESG criteria into their service provider selection processes. Back in 2021, PwC uncovered that 2/3 of the European banks they surveyed were already incorporating ESG requirements into their existing outsourcing relationships and in the selection process of new partners and service providers.

5. Intensifying regulatory pressures due to Basel IV

The Basel IV (or Basel 3.1) framework — a continuation and refinement of Basel III — began its phased implementation in 2023, and full adherence to the framework will be required by 2028. The new rules are intended to strengthen European banks' regulation, supervision, and risk management to ensure their resilience to economic shocks. European banking institutions need to prepare for these changes by enhancing their risk management practices and internal models and ensuring robust compliance mechanisms are in place.

As banks adapt to these requirements, they may need to reassess their capital allocation strategies, which could eventually reduce lending capacities or increase costs for borrowers to maintain compliance.

In addition, Basel IV emphasizes the importance of liquidity and stable funding, requiring banks to hold higher-quality liquid assets.

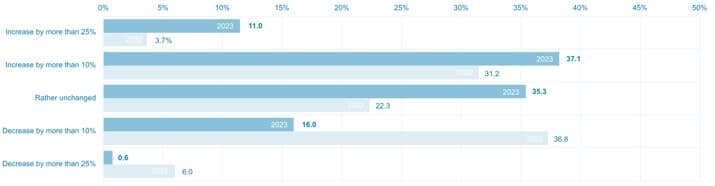

6. Resurgence of syndicated loans

The syndicated loan market in Europe is experiencing a resurgence in 2024, mostly on the back of refinancings, which are poised to become the key driver of market activity this year. A recently published survey by the Loan Market Association, the authoritative voice of the syndicated loan market in EMEA, revealed that +70% of market participants expect syndicated loan volumes to be stable or increase by more than 10% in 2024. The best opportunities are expected to lie with refinancings and restructurings.

This resurgence in the European syndicated loan market in 2024 is also supported by favorable competitive dynamics with private credit and a general rebound in market performance despite macroeconomic challenges. Also, with tighter capital requirements, banks might show a growing preference for shared lending risks. At the same time, benefiting from an increasingly competitive lending environment, borrowers are looking for innovative loan structures to meet their financing needs.

Source: LMA

7. Strategic cost management

In an era of economic recovery, where interest rates are adjusting from historical highs, sustainability goals and regulatory requirements are mounting, banks are focusing on strategic cost management rather than short-term cost-cutting.

This shift is crucial for maintaining profitability while investing in growth areas such as technology and sustainability, ensuring long-term resilience and competitiveness in the face of fierce competition from new entrants like neobanks and fintechs.

Strategic cost management for European banks means leveraging automation and advanced data analytics to reduce operational costs, re-evaluating branch networks, optimizing digital channels, enhancing process efficiencies, and outsourcing non-core activities to reach a sustainable cost structure.

Conclusion

As European corporate and commercial lending continues to evolve in 2024, several key trends are reshaping the landscape. From the easing of credit conditions and the adoption of advanced digital technologies to the increasing role of outsourcing and sustainable lending, European banks are adapting to new market dynamics and regulatory pressures. These shifts highlight the sector's resilience and its ability to embrace change—positioning itself for growth in a competitive, digitally-driven, and sustainability-focused environment.

Moving forward, the ability of banks to navigate the complexities of regulatory changes, digital transformation, and market demand will determine their success in capturing new opportunities. As they strategically manage costs, innovate with new technologies, and meet evolving customer expectations, European banks are set to play a pivotal role in driving the region's economic recovery and sustainable growth.

How Evalueserve Can Help

We partner with corporate and commercial banks to improve efficiency and accuracy and meet the demands of a changing market and heightened regulatory scrutiny. Our tech-enhanced services combine domain expertise with technology accelerators, such as AI-powered Spreadsmart, to help banks make faster, smarter credit decisions. We support major banks around the globe with solutions across the lending lifecycle, including:

Check out our blog Emerging U.S. Lending Industry Trends in 2024.

Sources:

https://hesfintech.com/blog/commercial-lending-trends-2024/

https://www.lma.eu.com/news-publications/press-releases?id=209

https://www.strategyand.pwc.com/de/en/industries/financial-services/outsourcing-banking.html

https://www.environmental-finance.com/content/downloads/sustainable-bonds-insight-2024.html

https://www.finastra.com/viewpoints/articles/esg-lending-what-banks-need-do-2024

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.