Aluminum production is estimated to account for ~3% of global emissions. The refining of alumina for the production of primary aluminum and smelting are responsible for 90% of the industry’s CO2 emissions. Furthermore, the production of the metal is responsible for nearly ~4% of global electricity consumption, which is at the center of global GHG emissions. These grim data highlight the need for immediate focus on production processes that will help clean the aluminum value chain.

But why is a shift to clean aluminum important? The need lies in the fact that the metal is vital for decarbonization efforts across industries. The World Bank has identified aluminum as a high-impact, cross-cutting mineral required in a wide range of technologies for decarbonization. Therefore, green aluminum is integral to enabling a decarbonized world.

The International Aluminium Institute (IAI) aims to establish a clear route for low-carbon aluminum production by 2030 by encouraging a switch to clean energy, a circular economy, and the adoption of emerging technologies. Coordinated efforts by governing agencies and industry players will be critical for a smooth transition.

Aluminum production and its environmental impact

The International Energy Agency (IEA) estimates that the aluminum industry was directly responsible for 275 million tons (mt) of direct (Scope 1) CO2 emissions in 2021. If indirect (Scope 2) emissions from energy consumed in production are factored in, the estimate swells to 1.1 Gigaton (Gt) of CO2 emissions, totaling ~3% of global manmade greenhouse gas (GHG) emissions. Moreover, ~56% of the global energy requirement for primary aluminum production is sourced from captive power generation, which connects a substantial part of indirect emissions to the aluminum industry.

Dependence on fossil fuels

Aluminum production requires the mining of bauxite, which is refined to alumina and followed by smelting to produce aluminum, which is finally cast and cut into various forms for different use cases.

1 2015 IAI average, 2 2020 global average, 3 2018 global IAI average.

Source: IAI

Smelting alone is responsible for emitting 12.8t CO2/t of primary aluminum, the highest among all steps involved in production. The IAI estimates that coal-based production emits 16.6t CO2/t aluminum produced, against 4t CO2/t by 100% hydropower-based smelters. Heavy dependence on fossil fuels for energy-intensive alumina refining and aluminum smelting is responsible for 90% of emissions across the value chain. Globally, ~57% of the energy used for primary aluminum is coal-based, a primary reason behind the heavy GHG emissions by the industry.

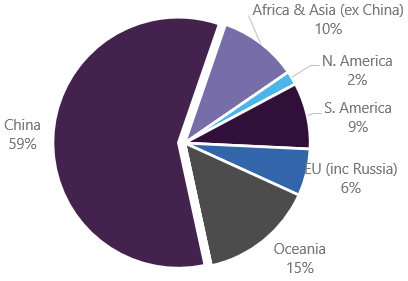

Concentration in China and dependence on captive coal power

While China accounts for over 61% of global aluminum production, the rest of Asia (ex-China) accounts for only about 9%. Of this, ~82% of production in China and ~94% in Asia (ex-China) are based on captive coal power, compared with ~4.6% in North America and ~1% in Europe.

Source: U.S. Geological Survey 2022

Source: U.S. Geological Survey 2022

Source: IAI

Source: IAI

Potential growth and need to clean aluminum production

About 72% of global aluminum demand originates from sectors that are critical to global decarbonization efforts, including transportation (26%), construction (24%), electrical (11%), and heavy machinery (11%). The IAI expects global aluminum demand to reach ~180mt by 2050 (~2% CAGR) up from ~100mt in 2021, supported by global economic and population growth. Furthermore, accounting for expected efficiency gains in aluminum usage, net global demand for the metal will likely reach ~150mt by 2050.

Role of aluminum in decarbonization technologies

The World Bank has identified aluminum as a cross-cutting mineral required across a wide range of technologies necessary for decarbonization. The production of aluminum required to advance these technologies could emit ~800mt of CO2, underlining the urgent need for clean aluminum production.

2DS = Scenario with at least a 50% chance of limiting the average global temperature increase to 2°C by 2100

Source: World Bank

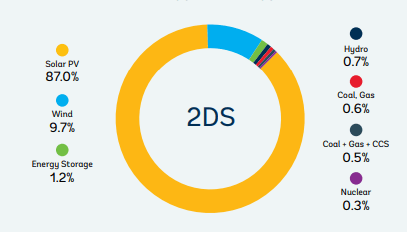

Cumulative global warming potential from extraction and processing of minerals, through 2050 under 2DS

Source: World Bank

Aluminum is a key material required for decarbonization, specifically for its role in electricity networks, solar PVs, EVs and energy battery storage, Concentrated Solar Power (CSP) deployments, and wind energy (refer to exhibit below). Overall, decarbonization deployment-related demand for aluminum is likely to reach ~30mt per annum or ~20% of net aluminum demand by 2050.

Source: IEA

Role of aluminum in decarbonization technologies

1. Electricity networks: Aluminum is a preferred material for overhead electricity networks due to its superior conductivity-to-weight ratio, compared with copper. The replacement, upgrade, and expansion of the existing electric network require aluminum. Similarly, setting up renewable energy infrastructure requires additional networks, which involve the use of aluminum. The IEA’s Net Zero Emissions by 2050 Scenario (NZE Scenario) estimates electricity networks to expand by ~165 million km by 2050, (~135 million km under the Announced Pledges Scenario (APS)). This expansion translates to a cumulative aluminum demand estimate of ~400mt and 500mt under the APS and NZE scenarios, respectively, by 2050.

2. Solar photovoltaics (PVs): Aluminum finds usage in solar PVs due to its high strength-to-weight ratio, conductivity, and corrosion resistance. According to the World Bank, aluminum accounts for 88% of the materials required for solar PV deployment, given its widespread usage in PV module frames, mounts, inverters, and cells. The IEA expects global solar power generation capacity, estimated at 751GW in 2022, to increase to ~11TW and ~15TW, respectively, under the APS and NZE scenarios by 2050. The cumulative aluminum demand estimate for solar PVs ranges from ~90mt (World Bank) to ~490mt (International Technology Roadmap for Photovoltaic).

Source: World Bank

Source: International Renewable Energy Agency (IRENA)

3. Electric vehicles (EVs) and batteries: The transport sector accounts for ~26% of global aluminum demand. The IEA NZE scenario estimates EVs to have a ~90% share in the auto market by 2050 (~90 million vehicles). Aluminum usage in EVs is higher than in conventional vehicles, owing to the metal’s light weight, which increases the driving range of EVs.

Aluminum is also used in Li-ion batteries, primarily as casing. It typically constitutes ~1/3rd of EV battery by weight. The IEA estimates that EV battery demand will reach 3.5TWh by 2030 under the APS scenario, six times higher than 550GWh in 2022. Under the NZE scenario, the demand is estimated at 5.5TWh by 2030. Based on the IEA’s expected ~90 million EV sales by 2050, aluminum demand for EV batteries will grow to ~5.4mt annually by 2050.

4. Concentrated solar power (CSP) panels: The use of CSP panels, which are more mineral-intensive than PV solar panels, is expected to increase in the future. With this, the demand for aluminum, which is used as a reflector in both tower systems and power blocks, is expected to go up from the current ~50kg AL / kWh capacity. The IEA expects CSP capacity to multiply 62 times from ~6.8GW in 2022 to ~320GW in 2050 under the APS scenario and 426GW under the NZE scenario, both of which indicate increased aluminum demand from the segment in the future.

The application of aluminum across these green tech sectors shows that its production and usage are likely to go up exponentially, highlighting the need to clean up the sector to meet the demands of a CO2-free world.

Approaches to aluminum decarbonization

The use of clean energy, recycling, and curtailing of direct emissions are some of the key modes of decarbonization of the industry. The IAI roadmap to decarbonization visualizes emission reduction of ~650mt CO2 from a switch to clean energy, nearly ~450mt CO2 from recycling, and ~230mt CO2 from improvement in production. Mission Possible Partnership (MPP), an IAI initiative on aluminum decarbonization states: “A clear route to market for low-carbon aluminum running at scale should be established by 2030 to give the right signals for a diverse set of production technologies for primary aluminum. The market should include demand-side commitments and carbon costs, with some support from policymakers for emerging technologies”.

Investment in decarbonization across the segment can be incentivized by strong penalties for non-adherence and premium of green aluminum. Moreover, institutional frameworks and policy support are paramount; financial institutions and the industry would be required to work together for a smooth transition.

Energy-based decarbonization

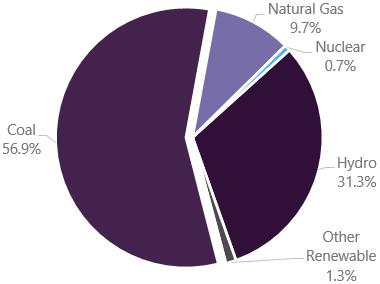

The use of clean energy sources is key to decarbonizing the aluminum segment. Smelters running on coal emits approximately four times the GHG emitted by those running on hydropower. Switching to gas-based production can lower emissions to 10.2t CO2/t of aluminum, low-emissions grid systems to 5.4t CO2/t, and hydropower to 4.6t CO2/t. Combining inert anode-based smelting with grid-based electricity can lower emissions to 3.1t CO2/t. However, as the IAI has estimated, almost ~67% of the power used for global smelting in 2021 was fossil fuel-based, (57% coal and 10% natural gas), and zero-emission sources made up the remaining 33% (31% hydropower, 1.3% renewables, 0.3% nuclear).

While switching to clean energy is an intuitive solution, the consistently high power load requirements of aluminum smelters and the unavailability of clean energy grids present a practical hurdle. The lack of adequate power can disrupt the smelting process and result in the solidification of molten alumina. Use of solar and wind power sources, as of now, are inadequate to cater to the requirements of smelters. Therefore, many aluminum smelters, especially in Asia, where grid systems are inadequate to cater to their power requirements, use captive coal power generation for smelting.

The IAI estimates that aluminum smelters will require ~1000tWh of low-carbon power by 2035. This indicates that the switch to clean power sources is likely to be a long-drawn process. Meanwhile, investment in low-carbon power sources is likely to be channelized through captive loop-hydro generation, CSP solar energy, and long-term PPA-based investments in clean energy projects and grids.

Decarbonization through recycling

Aluminum is an infinitely recyclable material with a scope of deployment across many use cases, barring a few like jet aviation and rockets. The energy requirement for recycled aluminum production is estimated to be 95% lower than for primary aluminum production. Moreover, recycled aluminum is estimated to generate little over 0.5t of CO2/t, a fraction of 16.6 CO2/t by primary aluminum production.

However, the current high rate of aluminum recycling in large economies and the emergence of new aluminum demand from decarbonization limit the potential for recycling as the only solution to the overall decarbonization of the industry. Current global post-production scrap collection stands at an estimated 95%, leaving little headroom for growth. The IAI envisages an increasing role of post-consumer scrap collection to fuel aluminum recycling. The agency targets a post-consumer scrap collection rate of 90% by 2050 (from 75% in 2022). It envisages that recycled aluminum will serve 54% of demand by 2050, up from ~36% in 2022, thereby stopping ~450mt of CO2 emissions annually (~40% of current emissions).

Technology-driven decarbonization

Promising technologies aimed at curtailing emissions are currently at an initial stage of development and are expected to come online by 2030. Some of the most promising technologies that could help reduce aluminum production-related emissions significantly are

- Mechanical vapor recompression (MVR): This technology aims to significantly reduce the need for energy and freshwater by using steam to heat caustic soda for the digestion of bauxite. Australia’s renewable energy agency is working on MVR, electric boilers powered by renewable energy and electric and hydrogen calcination, and believes it could eliminate ~98% of emissions associated with alumina refining.

- Inert anodes: Inert anode is a promising technology that offers to release oxygen instead of CO2 during smelting. Aluminum smelting uses carbon anodes that, on average, release ~2 tons of CO2/t of aluminum production. It is expected that one inert anode cell can generate the same volume of oxygen as 70 hectares of forest. Companies like Rusal have successfully tested inert anodes to produce 99% pure aluminum with an emission intensity of less than 0.01t of CO2/t of aluminum.

- Hal Zero: Norwegian aluminum and renewable energy company Norsk Hydro is developing this indigenous technology by converting alumina to aluminum chloride before electrolysis with the intent of releasing oxygen as the only emission. The technology aims to decarbonize aluminum smelting, eliminating emissions from both electrolysis and anode baking, resulting in emissions-free aluminum production.

In total, the IAI estimates ~230mt of CO2 emission reduction potential from technology and production improvements. It estimates that the additional cost of switching energy or adopting new technologies may range from USD275-725/t (average of USD400/t) depending on upfront capex, cost of technology, operating cost trade-offs, and location-specific availability of power alternatives. That said, the average cost is expected to peak in 2035 and trend downward thereafter, as the commercialization of technologies pave the way for better economics.

Policy action and institutional framework a must

Clear and stringent penalties on carbon emissions and premium pricing of green products can incentivize the aluminum industry to shift to lower emission production processes. A prominent EU policy, Carbon Border Tax Adjustment Mechanism (CBAM), proposes a carbon-footprint-based tax on materials imported into EU countries. The traceability of supply chains, including direct and indirect emissions related to aluminum imports, will gain relevance as the CBAM enters a ‘transitional phase’ in the second half of 2023 when the EU plans to introduce reporting obligations and test the CBAM without imposing any duties. The full implementation of the policy will begin in 2026.

Meanwhile, the Aluminium Stewardship Initiative and Metal Bulletin define aluminum produced with less than 4 tonnes of CO2 per ton as green, although products with much lower emission intensity exist. Clear policies and standards on categorizing green aluminum will aid the emergence of a true green aluminum and incentivize investment in decarbonizing the industry. However, given that the IAI estimates aluminum cleaning to involve a cost of USD400/t, the current 3-4% premium on green aluminum seems inadequate to drive a transition.

Aluminum decarbonization by mid-next decade

As aluminum production is a key source of global emissions and the metal plays a critical role in enabling decarbonized technologies, there is an urgent need for the aluminum value chain to be cleaned up. While changing the energy mix seems a logical solution, it entails cleaning the energy/power sector, which may be beyond the direct control of aluminum producers. Therefore, the deployment of clean aluminum production technologies and recycling are expected to lead the decarbonization drive, which may be followed by the decarbonization of power generation.

Technologies like ELYSIS, MVR, and inert anodes, which hold significant emission-reduction potential, are expected to see commercial deployment by 2030, although full-scale industry decarbonization is only expected to play out by the middle of the next decade. In the meantime, clear policy actions and institutional frameworks are required to commercially incentivize the industry to move to low-emissions production.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.