Much as we’d like to believe that billions and billions of stars can exist somewhere in an imagined universe, they need physical space, brick and mortar buildings, and real capacity to live. Just like our thoughts are housed in our brains with their intricate neural networks and gray matter, data and applications need physical homes to thrive. With the digital transformation that was accelerated by the COVID 19 pandemic and the technology explosion of Generative AI (GenAI), we find ourselves looking frantically for mega-capacity real estate for our changing digital needs.

As Abhinav Johri, EY India Technology Consulting Partner, put it, “with 80% of Indian organizations adopting the cloud to enable a range of business capabilities such as intelligent applications with Gen AI, native functional and data products, and highly intuitive orchestration platforms the imperative is clear: embrace the cloud not merely as a tool, but as an enabler of transformative change”

Against this backdrop, where do we stand with data centers in India? Every day, we’re inundated with investment-related newsflow about data centers. In this report, we explore the factors behind the growth of data centers in India. But first, an overview of the Indian data center market.

The Indian Data Center Market

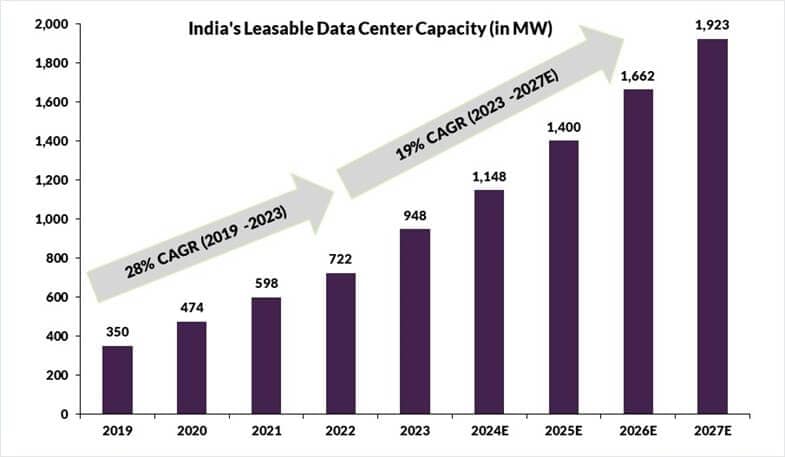

In the early 2000s, data center capacity (primarily measured in megawatts, MW) in India significantly lagged that of its G20 peers owing to an underdeveloped ecosystem. India’s first data center was set up in the early 2000’s and by 2019, India had amassed a capacity of only 350MW compared with its G20 peers such as China with 750+ MW, Australia with 800+ MW, Singapore with 520+ MW, South Korea with 580+MW, and South Africa with ~175 MW.

During the pandemic, there was a surge in “digital transformation” activities across the globe including India. Working from home and online classes for schools and colleges accelerated the adoption of over-the-top (OTT) services, e-commerce, social media, etc., boosting demand for digital services.

Given the sharp increase in digitization efforts as a result of the pandemic, the Indian government recognized the importance of data centers and introduced a “Draft Data Center Policy” in 2020 to make India a “Data Center Hub.” The policy addressed many important issues and has been instrumental in the development of the data center ecosystem and its expansion, with leasable data center capacity increasing at a 28% Compound Annual Growth Rate, or CAGR (from 350MW in 2019 [~2% of Global capacity] to ~950MW in 2023 ([~3% of Global capacity]). Over the same period, global data center capacity recorded an 18% CAGR to 34,000MW in 2023 from 17,500MW in 2019.

As per industry forecasts, data centers will continue to grow in India and reach more than 1,900MW of leasable capacity by 2027E (a ~19% CAGR over 2023-2027E), driven by:

• Growing mobile data consumption resulting from continued penetration of 5G services

• Increased adoption of OTT services • Rapid digitization of financial and healthcare services

• Establishment of a sovereign data center

• Data Privacy Laws

• Increasing adoption of Generative AI (GenAI) by Indian enterprises

We believe this capacity growth in India will far exceed the 1,900MW+ estimate; by 2027, data center capacity in India as a percentage of total global capacity will be in the low-single digits, while its contribution to total data generation will be much higher (20% of global data generation currently).

Factors Driving Data Center Growth in India

Mobile data consumption should increasingly rise due to continued penetration of 5G services. According to Nokia’s Mobile Broadband India Traffic Index, monthly mobile data consumption in the country increased to 17.4 exabytes in 2023 from 1.93 exabytes in 2017, i.e., a 44% CAGR. This growth was led by increase adoption of OTT services, affordability of data, higher prevalence of e-commerce platforms, and social media, among other drivers.

Bharti Airtel and Jio began offering 5G services starting in October 2022, which also led to 21% YoY growth in monthly mobile data consumption in 2023 (users of 5G services consume 3.6x times more data compared with 4G). In 2023, 5G traffic was 14.8% of total traffic (versus 1.7% in 2022), with the 5G user base being only 11%.

The greater availability of affordable 5G phones along with no differential pricing between 5G and 4G plans should drive accelerated adoption of 5G services in India, in turn driving a surge in data consumption. According to Ericsson Mobility, monthly data consumption in the India, Nepal and Bhutan countries is expected to be ~63 exabytes by 2030 (2024-2030E CAGR of 17%). We assume that the traffic growth for these combined countries to be a proxy for India’s traffic growth.

Users of 5G services will be using data-heavy applications including GenAI applications for daily tasks to improve productivity (AI apps such as Siri and Google Assistant are already contributing to a sharp rise in uplink traffic), High-Definition Gaming, AR/VR use cases, 4K- and 8K-enabled social and multimedia services, increased usage of collaboration platforms, and more, facilitating the need for data centers with high computing capacity.

Rapid Digitization of Financial and Healthcare Services:

Financial Services: India has witnessed rapid digitization of financial services in part due to the increasing use of technology/ IT by banks, FinTechs, and NBFCs to effectively cater to their customers’ needs. These digitization initiatives have helped the financial services sector to improve efficiency, reduce customer acquisition costs, create customer-oriented business models, and strengthen risk control measures. However, this rapid digitization is only the first step, and there is substantial scope for further digitization of services in India.

The Reserve Bank of India (RBI) released its Report on Currency and Finance on July 29, 2024, which highlighted the following areas that could be further digitized:

- During 2023-2024, the bank credit-to-GDP ratio was at 58.7%, leaving room for further financial deepening via financial innovations.

- Over time, the share of short-term maturity loans via Scheduled Commercial Banks (SCBs) has declined, providing opportunities for digital lending in small-ticket loans. Financial innovations that reduce loan-processing costs can help regulated entities (REs) penetrate this segment in collaboration with the FinTech industry.

- Underserved credit regions in the country offer opportunities for digital banking products and services. For example, credit from SCBs in rural areas (mainly tier 5 and 6 centers) and semi-urban areas (including tier 2, 3, and 4 centers) was 17.7% in 2023, leaving scope for additional growth via digitization.

Apart from these areas, banks are expected to continue to digitize their internal processes to reduce compliance costs and enhance customer experiences. They will also incorporate AI models in their credit lending business to improve their risk assessments at a low cost.

In a Sep 6, 2024 press release, the Chairman of the Indian Banks’ Association, M.V. Rao, emphasized the importance of continued digitization of financial services in India, noting that “to fuel inclusion and credit growth, we must continue to innovate and reimagine our deposit strategies, aligning them more closely with our customers’ evolving needs and preferences. This growth will be aided by our workforce’s full potential, which must be harnessed using digitisation and emerging technologies like GenAI.”

Digital Health Care Services (~USD48b in 2033, ~18% CAGR 2024E-2033E): To provide affordable healthcare to its large base of citizens, the Indian government envisioned a fully digitized healthcare system in 2017 via the National Health Policy. On Jan. 2, 2019, the National Health Authority was set up for the governance of e-health standards, privacy, secure storage, and exchange of health data. Furthermore, the Ayushman Bharat Digital Mission (previously titled the National Digital Health Mission) was created on Aug. 15, 2020, to provide quality, affordable healthcare accessible to citizens anytime and anywhere via online access to digital records.

As part of the Ayushman Bharat Digital Mission, Indian citizens need to generate ABHA, a unique healthcare ID, via which they can share their digital health records with hospitals, clinics, insurance companies, and other health-care-related institutions. The government is incentivizing hospitals, clinics, and insurance companies to upload digital healthcare data on its portal. There has been a widespread adoption of ABHA, evidenced by an increase in registrations and the number of online appointments booked through it. We expect this to rise further, necessitating an increase in data center capacity.

Indian Government to Establish Sovereign Data Centers: To efficiently roll out and adopt the National eGovernance Plan, the Government of India has identified the establishment of state data centers as a core infrastructure element. These data centers will function as a critical digital “nervous system,” enabling secure, 24/7 electronic delivery of G2G (Government to Government), G2C (Government to Citizen), and G2B (Government to Business) services. The central government has allocated a budget of approximately INR16.232b (~USD195m at INR84.07) for establishing these state data centers. Currently, the Government of India, through the National Informatics Center (NIC), is setting up national data centers to provide e-Governance services.

Moreover, the government is determined to create an ecosystem for AI use cases, approving the IndiaAI mission on March 7, 2024, with a budget of USD1.2b. The mission primarily aims to strengthen India's global leadership in AI. The government plans to establish a compute capacity with 10,000 GPUs via Public/Private partnerships, driving investment in and expansion of new data centers.

Heightened Compliance Regarding Data Privacy Laws

The Indian government passed the Digital Personal Data Protection Act, 2023 (DPDP) to safeguard the privacy of its citizens by regulating the processing of personal data. Although the DPDP Act provides freedom to process data outside of India, the government can restrict transfer/processing of data at anytime outside of the country. Moreover, if there is a data breach, the fine can be as high as INR2.5 billion (~USD30m at INR 84.07). The act also states that any other act with more stringent rules/regulation will supersede it. For example, compliance rules added by different government agencies promote localization of data, i.e., storage and processing of data in India. In the table below, we summarize the rules set by different government agencies:The Indian government passed the Digital Personal Data Protection Act, 2023 (DPDP) to safeguard the privacy of its citizens by regulating the processing of personal data. Although the DPDP Act provides freedom to process data outside of India, the government can restrict transfer/processing of data at anytime outside of the country. Moreover, if there is a data breach, the fine can be as high as INR2.5 billion (~USD30m at INR 84.07). The act also states that any other act with more stringent rules/regulation will supersede it. For example, compliance rules added by different government agencies promote localization of data, i.e., storage and processing of data in India. In the table below, we summarize the rules set by different government agencies:

|

Regulatory Entity/Act

|

Rules

|

|---|---|

|

SEBI

|

Regulated entities needed to store data within India.

|

|

RBI Data Localisation Law

|

Payment system providers must store all data in systems that are located within the Indian jurisdiction.

|

|

Companies Act 2013 (Sec 128)

|

Requires every company to keep books of accounts (including electronic form) at its registered office.

|

|

IRDAI

|

Storing and maintaining of records within India.

|

Source: Respective agency websites

Increased Adoption of OTT Services

India’s base of OTT subscribers grew from 335+ million in 2019 (a ~25% penetration rate) to 460+ million in 2023 (a 33% penetration rate), attributable to affordable 4G mobile phones and the diversity of content for users on the go. By 2025, OTT subscribers in India are estimated to reach 550 million (a 38% penetration rate), driven by premium 4K and 8K content at affordable prices on OTT platforms, penetration of 5G services, and affordable devices (5G handsets, TVs, etc.,) supporting 4K and 8K. The high-definition 4K and 8K content will require both computing and storage facilities, two of the primary drivers of data centers.

Growing Adoption of GenAI by Indian Enterprises

GenAI is already a revolutionary technological development in countries across the globe, and India is no exception. Many Indian enterprises have integrated or are looking to integrate GenAI into their business processes to enhance productivity and create new revenue streams. According to an IBM report (IBM Global AI Adoption Index 2023), about 59% of enterprise-scale organizations (over 1,000 employees) surveyed are actively using AI in their businesses, and about 74% of the early-adopter enterprises have accelerated their investments in AI in the past 24 months in areas such as R&D and workforce reskilling.

According to NASSCOM, “India’s 2024 AI adoption index score is 2.47 on a 4-point scale, compared with 2.45 in 2022, and 87% companies are in the middle stages of Enthusiast and Expert AI adopters.”

All these factors call for GenAI to be at the forefront for Indian enterprises. This adoption of GenAI will have ripple effects on data center demand because computational power is needed to train the large language models (LLMs), which can only be met via data centers.

Government Policies

Policies Encouraging Robust Growth in Data Center Investment Across India

In-line with the Government of India’s Draft Data Center Policy 2020, many state governments have come up with policies that facilitate data centers to be set up without any hassle and operate smoothly. These policies have addressed issues related to land acquisitions, 24X7 availability of power and water resources, tax incentives, etc., and bode well for substantial investment, with industry experts expecting more than USD20b worth of investments in the next five to six years.

Hyperscale players such as Amazon and Microsoft have announced big capital expenditure/investment plans for setting up data center regions in India in the coming years. Amazon plans to invest USD4.4b by 2030 and Microsoft ~USD2b in the next 15 years. The favorable government policies have aided established companies entering the Indian market via M&A (e.g., in September 2021, Equinix, one of the largest global co-location companies, entered India via the acquisition of two data centers in Mumbai for USD161m and has been expanding its capacity further) and JVs (e.g., in July 2023, Digital Realty, the largest global provider of cloud- and carrier-neutral data center, entered the Indian market via a JV with Brookfield and Jio under the name of Digital Connexion, with initial plans to develop land in Chennai and Mumbai).

Below, we highlight the incentives that state governments are providing for securing robust investments in data centers:

Data Center Construction Cost Is Lowest Among APAC Peers

According to a Cushman and Wakefield report, the construction cost in India is the lowest at USD6.8m/MW, compared with its APAC peers, including Australia (USD9.17m/MW), Japan (USD12.73m/MW), Singapore (USD11.23m/MW), and China (USD6.84m/MW). This low cost is attracting substantial investments in data centers throughout India.

Shortage of Power Supply Could Hinder Data Center Growth: Data centers are known to be “power hungry.” With the advent of GenAI use cases, the demand for power has grown exponentially, despite technological advancements. Marc Garner, SVP Secure Power Europe at Schneider Electric, highlighted that “creating GPT-3 consumed 1,287 megawatt hours of electricity and generated 552 tons of CO2—the equivalent of 123 gasoline-powered passenger vehicles driven for one year. What’s more, data centres are adopting high-density racks that can accommodate a larger number of servers in a smaller space, further driving up power requirements.”

In the U.S., data center hubs like Ashburn and Nova are facing a shortage of power supply for the expansion of new data centers, coupled with a surge in power prices. Globally, power prices have increased in many markets; however, India is an exclusion to this trend, in part due to government strategies promoting the establishment of data centers. However, if global power supply shortages impact India in the next couple of years, it could significantly hinder the growth of this industry in the country, despite the positive factors previously mentioned.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.