Fund Finance: A Crucial Revenue Driver in the Post-Financial Crisis Era

"Liquidity is the currency of bear markets," as stated by Laurent Bernut, holds particular significance for the Alternative Investment Funds (AIFs), which typically invest in a variety of asset classes, including Private Equity (PE), Hedge Funds, Real Estate, Commodities, and Derivatives. Following the 2008 global financial crisis, the AIF market experienced significant growth, and fund finance emerged as a crucial financial instrument for investment funds to manage their capital structure, operations, and investments. The growth of the AIF market provided banks with a new revenue stream by providing liquidity to the rapidly expanding world of alternative financing.

The use of fund facilities in alternative investments can be traced back to the early days of private equity and hedge funds. As these investment vehicles grew in complexity and size, fund managers sought innovative solutions to address operational and liquidity challenges. However, it was after the financial crisis that banks, faced with regulatory bans and higher capital requirements, had to find new and safer income sources. This led to a surge in alternative fundraising, driven by investors’ search for uncorrelated assets offering attractive risk-adjusted returns in a low-yield environment. This development became a major revenue driver for both banks and non-bank lenders.

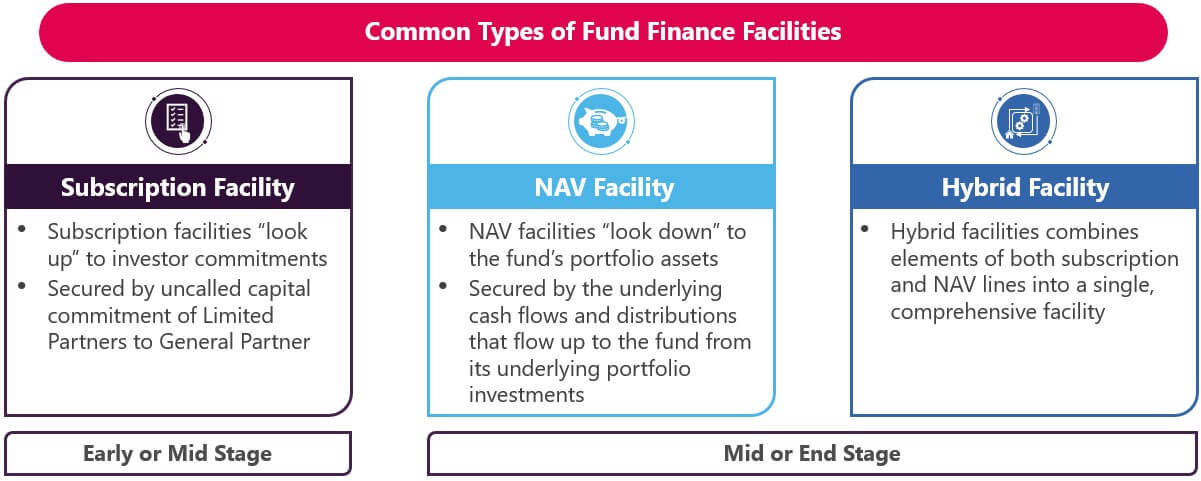

Over time, fund finance has evolved from simple bridge-type subscription facilities to a sophisticated product offering various financing options at the fund level such as Net Asset Value (NAV) facilities, showcasing the adaptability of the industry.

Products Utilized at Different Stages of a Funds Life

The Role of NAV Facilities in Fueling Growth

Subscription facility, also known as capital call facility, was once a niche product but has now become a widely used portfolio management tool, with over 90% of PE funds utilizing this facility. Fitch Ratings estimated that the subscription finance market stood at approximately $750 billion at the end of 2022. Now, lenders are shifting their focus towards driving value creation through extended hold periods using fund-level NAV facilities. NAV finance has seen significant growth in recent years, fueled by the expansion of the PE market and a rising demand for additional liquidity sources. NAV facilities allow general partners (GP) to borrow against the NAV of their fund’s assets. This enables managers to make distributions to limited partners (LP) without exiting valuable assets and provides additional financing options for portfolio companies after the fund’s investment period expires.

The chart below illustrates the Assets Under Management (AUM) of private equity funds that are beyond their investment period – the target market for NAV finance – indicates significant growth potential for NAV facilities.

However, the collapse of major U.S. subscription credit facility providers in 2023, such as Signature Bank and First Republic Bank, had a substantial impact on lending capacity. Additionally, increased base rates in the U.S. and a slowdown in fundraising raised uncertainties about the future of fund finance. In response, lenders are adopting a more selective and strategic approach, leading to discussions on adapting lending practices to current market dynamics. To navigate these challenges, lenders are exploring innovative solutions, such as “hybrid” facilities underwritten based on both investors’ capital commitments and investment portfolios. The year 2024 might be challenging, but has an opportunity for those who are visionary, experienced and have a strategy to deal with such scenarios. Nevertheless, the fund finance market continues to evolve, with a focus on adapting to market dynamics and regulatory shifts.

Navigating Regulatory Shifts with Subscription Facility Ratings Strategy

Financial institutions are facing a new regulatory landscape as the U.S. regulators are preparing to increase risk weighted asset capital requirements. These higher capital requirements aim to enhance financial stability and resilience within the industry, ensuring that institutions have sufficient capital buffers to withstand potential economic downturns or market shocks. While higher capital requirements may initially pose challenges for fund finance providers, there is a potential for strategic adaption.

One way to mitigate the impact of increased capital requirements is by utilizing new subscription facility ratings. By obtaining favorable ratings for these facilities, financial institutions have the potential to reduce their overall capital requirements. This is because the lower risk associated with rated facilities allows for a more efficient allocation of capital. In 2023, Fitch made a significant advancement in evaluating fund finance instruments by introducing subscription facility ratings, which they plan to extend to cover NAV facilities. This expansion marks a significant milestone in the development of fund finance ratings and demonstrates a growing recognition of these financing instruments within the broader financial ecosystem.

The implementation of ratings can offer several benefits beyond capital relief. It enhances transparency and risk management practices, providing investors with greater insight into the credit quality of fund finance portfolios. As more ratings agencies publish their methodologies for subscription facilities and GPs consider their stance towards external ratings, the landscape of fund finance ratings is expected to evolve further.

Fitch Rating Process for Subscription Finance Facilities (SFF)

Exploring the Pros and Cons of Fund Finance

The rapid growth in fund finance stems not only from attractive market opportunities, but also from the compelling benefits associated with lending facilities, including:

Low Credit Risk: Fund finance products are typically well-collateralized, mitigating credit risk for lenders. These loans are often secured by the assets of investment funds, such as their investment portfolio, uncalled capital commitments from investors, or management fees. In the event of default, collateral can be liquidated to recover outstanding payments. Furthermore, personal guarantees from the general partner or limited partners can serve as a fallback option.

Diversification: Lenders can diversify their lending portfolios beyond conventional loans by extending financing to funds with diverse investment strategies and asset classes. Diversifying into these investment funds enhances portfolio resilience and stability, especially during periods of market volatility.

Higher Return: Fund finance offers the potential for higher returns compared to investment-grade products, thereby enhancing the overall profitability of lenders’ portfolios.

However, fund finance also presents several challenges. Managing data is a significant obstacle, as traditional risk management systems are not adequately equipped to handle it, underscoring the need for specialized risk management tools or purpose-built software solutions. Some of the main challenges lenders usually encounter for this product are:

Exposure Management: Although a fund facility may seem diversified due to exposure to various investors, it could significantly overlap with other facilities held by the lender. Therefore, in contrast to traditional lending models, where counterpart exposure suffices for risk assessment, fund finance requires the capability to evaluate exposure to individual investors or their parent entities across numerous facilities to effectively manage concentration risk. However, lenders face difficulty in aggregating and analyzing data as borrowers often provide information in varying formats, including PDF and Excel files. Furthermore, discrepancies in data entry methods or variations in naming conventions across diverse sources add to the complexity of the task. For example, one source might use abbreviations, while another spells out words in full, leading to variations in the data. Addressing these challenges often involves cleaning and normalizing data for better analysis and decision-making.

Analyzing Trends and Validating Data Integrity: Analyzing historical trends of collateral or borrowing base can be challenging. This involves processing large volumes of data to identify patterns, assess risk, and make informed lending decisions, requiring sophisticated data analytics capabilities. Concurrently, it is crucial for lenders to ensure that the amount of credit extended is properly collateralized. This includes verifying complex borrowing base calculations, such as concentration limits, advance rates, and the inclusion of eligible investors. Failure to conduct thorough verification can expose lenders to heightened risk of losses in the event of default.

Laborious Credit Review Process: Lenders need to assess the creditworthiness of their borrowers during both prelending and portfolio management phases to ensure that loans are issued to reliable borrowers and to minimize the risk of default over time. However, these assessments are very time-consuming, encompassing spreading financial statements, performing variance analysis, collateral valuation, verifying covenant compliance, and preparing detailed qualitative reports. This labor-intensive work requires skilled personnel and considerable efforts.

Summary

Fund finance lending plays a crucial role in providing liquidity and flexibility to investment funds, allowing them to efficiently manage capital flows, leverage investments, and enhance overall returns. As the investment fund industry continues to grow and diversify, the demand for fund finance facilities is expected to increase, leading to a substantial rise in overall exposure. This trend underscores the importance of robust and efficient credit management processes to mitigate risks and support sustainable growth.

Currently, many aspects of the fund finance lending process are manual, which can be time-consuming, prone to errors, and inefficient. This creates a significant opportunity for improvement through automation and specialized support services. Firms like Evalueserve offer comprehensive solutions to streamline and manage the credit lifecycle for fund finance facilities. By leveraging advanced analytics, automation, and industry expertise, Evalueserve can help financial institutions enhance their operational efficiency, reduce risks, and provide better service to their clients.

In summary, as fund finance lending continues to gain significance in the investment fund industry, it is imperative for financial institutions to employ innovative solutions to efficiently handle the credit lifecycle. This will be essential for meeting the rising demand and staying ahead in the competitive landscape.

How Evalueserve Can Support Lenders in Managing Fund Finance Portfolios

Case Study: Accelerating Fund Finance Monitoring by 70% Through Automated Borrowing Base Document Processing

Problem Statement: The legacy process of fund finance reporting in the corporate banking division of a top 10 North American bank was highly manual with approximate lead time of three weeks. The bank receives borrowing base documents from approximately 40-50 borrowers each month, which are processed manually to assess credit risk and ensure compliance with lending limits. The documents arrive in diverse formats, including PDFs and Excel spreadsheets, each with varying structures and data points. This labor-intensive process involves data extraction, standardization, and verification of the calculations. The manual process leads to delays in reporting and increases the likelihood of inconsistencies and errors.

Solution: Based on our feasibility study, we concluded that an automated solution could efficiently process borrowing base documents, reduce processing time, and ensure accurate, timely exposure reporting. Leveraging cutting-edge technology, Evalueserve engineered an automated solution, enabling seamless consolidation of data from diverse sources, while accurately calculating indirect exposure to investors and their parent entities across all funds.

Benefits: The implementation of this tool has yielded 70% time saving for this work scope, including swift and efficient data retrieval with a single click, mitigated risk of manual errors, and substantial time savings. With intuitive data filtration widgets embedded in the dashboard, stakeholders can also customize their views and gain enhanced capabilities for reporting and risk assessment. This level of flexibility empowers lenders to tailor their analysis to specific needs and quickly identify potential areas of concern. In addition to the technological advancements, our team of experts plays a crucial role in supporting our clients. They conduct monthly reporting and provide invaluable insights derived from their extensive experience in the field, further empowering our clients in their decision-making processes.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.