Global Financial Services Market 2024: Rate Cuts to Recovery

In 2024, the global financial market was eagerly awaiting a “rate cut to recovery” in midst of stable inflation and slower growth of the major economies. The Federal Reserve in the US led the way in the second half of the year, reduced their interest rate three times by a total of 1.0% from its peak. This was the first rate drop since the early stages of the COVID-19 epidemic. The previous “higher for longer” interest rates had caused property values to decline, which in turn has severely impacted the banks and borrowers. The current rate cycle should see lower lending rates, which is expected to lead to greater leverage ratios and M&A valuations, particularly for LBOs. As in the past, lower rates and higher multiples are expected to encourage more M&A activity, particularly as the current environment appears to be more favorable than in the previous two rate cut periods.

Geopolitical risks continued to be high, as there remained policy uncertainty due to the super-cycle of global elections. All these factors continued to cause volatility in the financial market and thereby created an environment of uncertainty regarding the future of the global economy during the year.

Furthermore, the financial services (FS) sector was subject to other industry-specific issues, such as pressure on costs and asset quality, as well as uncertainty surrounding global central banks' interest rate policies. These factors collectively put a burden on the profitability and equity of FS businesses. In such a complex scenario M&A served an integral part of the transformation process across the sub-sectors with dealmakers focusing on enhancing capabilities and driving future growth in the given current socioeconomic climate were organic growth faced serious headwinds.

Recent boardroom discussions highlight that dealmakers are mostly optimistic about the medium-term M&A picture which is expected to remain profitable and relevant due to pressures induced by digitalization, questions on sustainability and current workforce challenges globally.

We anticipate that strategic purchasers will carry on with their practice of making bolt-on, lower-value purchases in 2025 to enhance their current product and geographic portfolios. In the FinTech industry we expect strategic buyers' venture arms will continue to take minority investments in FinTech companies.

The following key developments had a strong bearing on M&A and Capital markets’ activities across the global financial services market during 2024:

- Companies explored foreign investments to bring in cutting-edge technology, global best practices, increased product offerings and improved access to capital for the next level of growth.

- While several investment grade companies borrowed to seek high-value targets throughout the quarters, numerous bigger companies took advantage of attractive valuations to finance huge deals.

- Structured deals, which include spin-offs, separation, and carve-out transactions, also drove volumes.

- While macroeconomic conditions and geopolitical tensions remained challenging, recent gains in the financial markets and reduction of interest rates from central banks revived investor confidence.

- Spotlight were also on divestitures of non-core assets as businesses attempted to strengthen their balance sheets and make their business models more resilient.

- The focus seemed to be shifting to long-term planning and M&A as a way of addressing strategic issues in the sector, leading to a return of investor confidence and stability to banking markets.

Despite ongoing challenges, the Fed’s rate cut, strong corporate earnings, and resilient consumer spending helped the market reach new highs in 2024

Key Sectoral Performance: Tale of 4 Key Sub-Sectors

Banking

- The M&A deal volume improved in 2024 compared to 2023 but remained slow due to uncertainties connected with interest rate developments, evolving capital regulations, more regulatory scrutiny of mergers, and potentially increasing risks in loan books, particularly around commercial real estate

- In the US, 46 transactions took place in the Midwest, making it the most-targeted region, followed by the Southeast region with 23 announced transactions

- US bank M&A activity is anticipated to increase in 2025 because of the recent decrease in medium-term interest rates, with multiple US banks already expressing interest in pursuing M&A agreements

Asset Management

- Companies are focusing more into strategic alliances to optimize cost structures in addition to growing revenue.

- Traditional active managers are expected to collaborate to scale up to fund new capabilities (such as ESG) and boost distribution.

- Mergers and acquisitions with direct pension fund involvement soared high in the second quarter of 2024 • The Wealth Management M&A market remains strong, with 336 transactions completed in 2024.

- Private equity-backed acquirers continue to play a pivotal role in the market, accounting for 77% of acquisition in 2024.

- Asset management business volumes are expected to continue to rise because of the potential for a minor reversal of macroeconomic conditions and future interest rate reductions

Insurance

- Insurance corporations continue to divest capital-intensive life and annuity businesses to focus on core products and reduce complexity in their operations.

- As per OPTIS Partners, there were a total of 750 announced insurance agency mergers and acquisitions in the 2024, down 10% from 833 in 2023.

- Insurance companies are collaborating with InsurTechs to take advantage in areas such as machine learning and artificial intelligence capabilities.

FinTech

- Despite growth in broader venture funding, fintech funding declined by 20% in 2024, compared to 2023.

- The total capital invested in fintech globally were amounted to $43.5bn in 2024, compared to $54.2bn in 2023.

- Although private equity is making fewer bets, they are increasing in size as late-stage fundraising rounds become the primary focus of investment.

- Significant developments in blockchain, digital banking, mobile payments, cybersecurity, and API integration will start to emerge soon

Global Financial Services M&A 2024: Fireworks as Market Rebounds!

Recent improvements in liquidity and economic conditions drove a rebound in M&A activity in 2024. Global M&A activity increased by 43% in 2024 (soft comparable), driven largely by the US and European big-ticket acquisitions. During the year, several large companies capitalized on strong valuations to finance big deals, while some investment grade companies borrowed to pursue high-value targets. US-based companies accounted for a larger part of world-wide deals in 2024. As the economies in Europe continue to grow and market confidence improved further due to anticipated additional interest rate reductions, M&A deal activity rebounded significantly in 2024 vs y-o-y. Deal activity in APAC improved however was negatively impacted by lower volumes in China and Southeast Asia, partially offset by a surge in deals in India.

While a miraculous cross-sectoral upturn in M&A activity might be challenging, there were some encouraging signs for possible deal-making, such as the recent rapid upturn in FinTech and InsurTech M&As.

Private equity (PE) players shifted their attention on conducting portfolio reviews, carrying out bolt-on acquisitions and making investments in cloud transformation, data and analytics capabilities. Additionally, dealmakers anticipate a further increase in M&A volumes from activist campaigns in the upcoming quarters due to prior challenging growth factors, which had already provided a chance for some notable activist investors to start new proxy battles.

Mergers and acquisitions rebounded in the 2024 after a downbeat in 2023, thanks to the return of mega deals.

Discover Financials’ acquisition by Capital One for $35.2bn and Haitong Securities by Guotai Junan for US$14.6bn were some of notable big-ticket deals (where the transaction value is greater than or equal to US$1.0bn) in 2024.

Some of the key observation during 2024:

- Steady flow of carve-outs, spin-offs and joint ventures offered creative ways to achieve strategic goals.

- Due to strict merger scrutiny by the regulators the buyers had to wait longer for deal negotiations.

- Corporates with strong balance sheets and sound M&A processes had a competitive advantage in the current market as they had the enough dry powder and the ability to extract synergies.

- Activism remained a significant factor, with many campaigns pressing for M&A transactions to enhance shareholder value.

- To finance significant deals, PE players combined financing mechanisms such term loans, seller notes, all-equity funding, earn-outs, consortium deals (including with sovereign wealth funds, pension funds, and family offices), and minority investments.

Key M&A Themes

Strategic Alliances

Banking Consolidation

Business Expansion

Refinancing

Boosting Market Share

Operational Synergies

Accelerated Digitization

Enhancing Capabilities

Funding: Volumes Rebounds as Optimism Grips the Market

The Debt Capital Market (DCM) showed high optimism in 2024 despite significant challenges and a global election “super-cycle” with 60+ countries go to polls. Issuers largely been able to push out near-term maturities amid tight credit conditions. Most of the deals were related to refinancing and repricing which were driven by the lack of new supply. Investors also exhibited greater risk tolerance as banks have been more active, resulting in increased M&A financing in the syndicated debt markets and more favorable pricing during the year. Aided by strong investor interest and tighter spreads, borrowers refinanced more costly private credit with more affordable widely syndicated loans. Overall, looking ahead we expect refinancing deals to remain under focus in 2025 with interest rate cuts and Central Bank stimulus globally, likely to give an improved market tone for deals offset a bit by some political headwinds.

The resurgence in Equity Capital Market (ECM) in the US was primarily driven by the perception of lower in interest rates and easing inflation, strong base effect (soft y-o-y figures) and better economic growth prospects and listing companies’ willingness to accept valuation resets. Majority of the deal activity came from FinTech companies with investors focusing on innovation and growth. The IPO backlog continues to be robust with a large set of companies planning to get themselves listed as post market performance improve. This should ideally continue to drive volumes in the 2025.

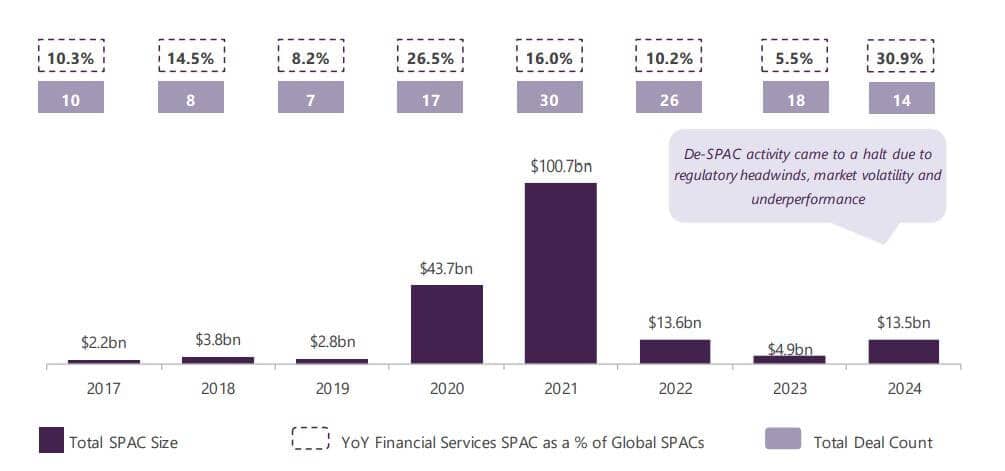

SPACs: Innovative Deal Structures are the Need of the Hour

The Debt Capital Market (DCM) showed high optimism in 2024 despite significant challenges and a global election “super-cycle” with 60+ countries go to polls. Issuers largely been able to push out near-term maturities amid tight credit conditions. Most of the deals were related to refinancing and repricing which were driven by the lack of new supply. Investors also exhibited greater risk tolerance as banks have been more active, resulting in increased M&A financing in the syndicated debt markets and more favorable pricing during the year. Aided by strong investor interest and tighter spreads, borrowers refinanced more costly private credit with more affordable widely syndicated loans. Overall, looking ahead we expect refinancing deals to remain under focus in 2025 with interest rate cuts and Central Bank stimulus globally, likely to give an improved market tone for deals offset a bit by some political headwinds.

The resurgence in Equity Capital Market (ECM) in the US was primarily driven by the perception of lower in interest rates and easing inflation, strong base effect (soft y-o-y figures) and better economic growth prospects and listing companies’ willingness to accept valuation resets. Majority of the deal activity came from FinTech companies with investors focusing on innovation and growth. The IPO backlog continues to be robust with a large set of companies planning to get themselves listed as post market performance improve. This should ideally continue to drive volumes in the 2025.

ESG: Key to Long-term and Sustainable Value Generation

The COVID-19 pandemic has demonstrated that adhering to ESG factors is key to crisis-resilient long-term value creation. Companies with dynamic business cultures were relatively more resilient during the shutdowns, given their ability to absorb the shock. Globally, investors have started to recognize the potential benefits of announcing an acquisition that is ESG accretive.

Global financial regulators have identified scenario analysis as a potentially useful means of evaluating and managing financial institutions' exposure to climate-related financial risks. Regulators in the US have begun to investigate how to use scenario analysis to better evaluate the long-term, climate-related financial risks that financial institutions face, as well as how these risks may emerge and vary from past events.

As the ESG investment market continues to grow rapidly, Banks are strategically deploying fintech ecosystems to drive sustainability in their products and operations which is referred to as ‘Sustainable Digital Finance’. Several banks have joined the UN-convened Net-Zero Banking Alliance. Under this, they have committed to align their lending and investment portfolios with net-zero emissions by 2050.

2025 Outlook: Spotlight on Adaptability and Rebuild

Despite the recent slowdown, the long-term fundamental M&A themes remain intact. We foresee the following trends to define the overall deal-making in 2025:

- Digital payments: Despite the ongoing macroeconomic difficulties and their implications on the M&A market, the payments sector continues to be quite appealing for the investors. The payments business is seen as more profitable, scalable, and less regulated than other areas of the financial services industry by corporates in the banking and payments sectors as well as private equity firms.

- ESG: ESG factors are becoming increasingly important to investors when making judgments about investments and formulating company plans. They have refocused their attention from asset managers and insurers on the ESG risks in their private investment portfolios due to recent geopolitical tensions.

- Emerging markets are expected to become centers for FinTech: Global governments will make more investments in South-East Asia, the Middle East, and Africa to expand their fintech ecosystems and bolster the regions' digital economies.

- Restructuring: Participants in the FS market are observing increasing indications of a decline in credit quality. They anticipate restructuring, such as the sale of non-core assets or non-performing loans (NPLs), to bolster balance sheets and raise capital ratios in the banking industry.

- Digital transformation: Digitalization and artificial intelligence (AI) continue to be strategic goals for financial services players to address consumer expectations and establish market position. Transaction activity in 2025 is expected to focus on deals to leverage data, implement solutions to growing cybersecurity concerns, drive operational efficiencies, and expedite transaction process.

- Private Equity: Insurance brokerage, platforms, fintech, insurtech and regtech are expected to be in the crosshair of deal makers. We therefore anticipate more M&A activity in these sectors as increased cost of capital and restrictions on leverage putting pressure on returns for PE investors, value creation will be more crucial than ever.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.