Highlights – Q1’24

M&A volume picks up while number of deals falls to nine-year low

M&A activity by the number of deals announced declined by 31% to 10,724 across the globe in Q1’24, compared with 15,532 in Q1’23, marking the lowest quarter for deal making since 2015. However, Q1’24 witnessed a 38% YoY increase in deal value to USD 798 billion, making it the strongest opening quarter for deal making across the world since Q1’22.

Region-wise, M&A activities in the US and Europe were up by 78% and 58%, respectively, on a YoY basis with US accounting for 61% of total deal volume, registering a 35 year high. However, Q1’24 was the slowest opening quarter in APAC since 2013, with a decrease of 28% YoY in overall M&A activities. High inflation and interest rates and geopolitical tensions continued to weigh on M&A activities globally. In sectoral trends, the energy and power and technology sectors led the mix, accounting for 18% and 16% respectively.

Debt capital markets remained solid

In Q1’24, global debt capital market (DCM) activity stood at USD 2.9 trillion, up by 16% compared with Q1’23, making it the strongest opening period for DCM activity since 1980. Meanwhile, new DCM offerings increased by 7% YoY to an all-time high. During Q1’24, investment-grade corporate debt issuances were up by 22% YoY while high-yield activity nearly doubled, compared with Q1’23 level, marking a three-year high. Green bond issuances totaled USD 144 billion, up by 11% YoY, making it the largest quarter for green bond issuance by volume on record. In sectoral activity, the consumer products, industrials, and media and entertainment registered double-digit percentage increases, compared with Q1’23 levels. However, technology was the only sector that witnessed a decline during Q1’24.

ECM activity reached three-year high

Global equity capital market (ECM) activity stood at USD 141 billion in Q1’24, up by 1% YoY, marking the strongest opening period for global ECM activity in three years. The US accounted for 40% of the overall issuances, with proceeds nearly doubled compared with Q1’23. ECM in China fell by 84% YoY, marking the lowest percentage of global ECM during Q1 since 2006. Global IPOs, excluding SPACs, stood at USD 21 billion, down by 16% YoY, marking the slowest opening period for global IPOs since 2019, despite a strong show from US listings, which more than tripled in the same period. Convertible offerings, which stood at USD 24 billion, were down by 6% YoY and accounted for 17% of the overall ECM activity. Technology, materials, and financials were the most active industries and together accounted for 63% of the overall issuance of convertible offerings.

Top five M&A deals

|

Date of announcement

|

Acquirer’s Name

|

Acquirer’s Location

|

Target

|

Target’s Location

|

Value (USD billion)

|

Target’s Industry

|

Deal type

|

|---|---|---|---|---|---|---|---|

|

Feb 19, 2024

|

Capital One Financial

|

US

|

Discover Financial Services

|

US

|

35.3

|

Financials

|

Stock

|

|

Jan 16, 2024

|

Synopsys

|

US

|

Ansys

|

US

|

32.5

|

Tech

|

Cash & stock

|

|

Feb 12, 2024

|

Diamondback Energy

|

US

|

Endeavor Energy Resources

|

US

|

25.8

|

O&G

|

Cash & stock

|

|

Mar 28, 2024

|

Home Depot

|

US

|

SRS Distribution

|

US

|

18.3

|

Retail

|

Cash

|

|

Jan 9, 2024

|

Hewlett Packard

|

US

|

Juniper Networks

|

US

|

13.6

|

Tech

|

Cash

|

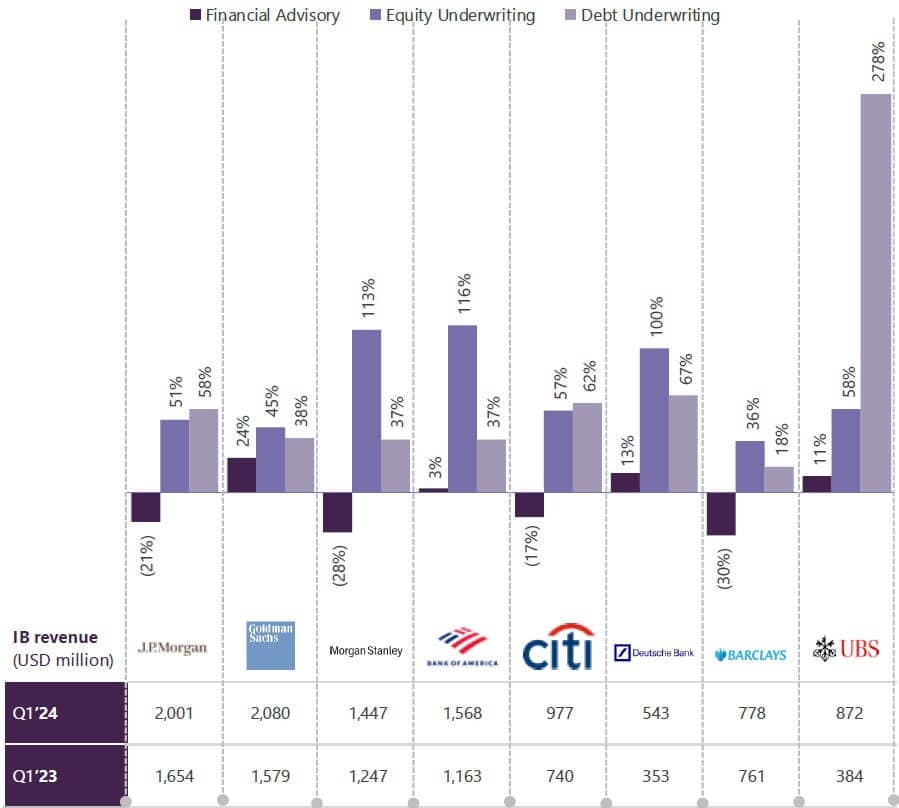

Unfavorable market continues to create headwinds for global investment banks

Investment banking (IB) revenues of major banks witnessed a revival in Q1’24, due to improving market conditions globally, leading to a sharp uptick across equity and debt underwriting businesses. A revival of mega deals, improved boardroom confidence on the back of strong earnings, potential interest rate cuts this year and an ebullient market were the main factors responsible for the bounce back. Market performance is expected to improve in 2024, due to pent-up demand for M&A and a strong pipeline, provided the macro environment remains stable.

Note: Revenues for Deutsche and Barclays were converted into USD using the exchange rate as of Mar 31, 2024; Revenue for Deutsche Bank reflects revenue from Origination & Advisory services; Revenue for UBS represents standalone for Q1’23, and for Q1’24 represents proforma for Credit Suisse post completion of acquisition in June 23

Bulge bracket investment banks – Performance highlights

JP Morgan’s IB revenue and fee were up by 27% and 21% YoY in Q1’24, driven by higher debt and equity underwriting fees, which were partially offset by low advisory fees. In the advisory segment, fees were down by 21%, driven by fewer large deals completed. The underwriting fees benefited from improved market conditions, with debt and equity up by 58% and 51%, respectively. In terms of outlook, it was encouraging to see some positive momentum in the announced M&A in Q1’24. However, it remains to be seen whether the momentum will continue and the advisory business will face structural headwinds from the regulatory environment.

Goldman Sachs’ IB fees increased by 32% YoY in Q1’24, reflecting significantly high net revenues in debt underwriting, primarily driven by leveraged finance activity in advisory (reflecting an increase in completed M&A transactions) and equity underwriting (primarily from initial public and secondary offerings). The bank tops the league tables for announced and completed M&A. Also, its backlog fell on a quarter-on-quarter basis, as it successfully brought transactions to the market, though client engagement and dialogues remain robust. Also, the firm expects positive growth in debt underwriting activity to continue this year.

Morgan Stanley’s IB revenue increased by 16% YoY in Q1’24, driven by a pickup in equity and fixed income underwriting-supported results, offsetting a year-on-year decline in the advisory business. The bank’s advisory revenues reflected a decline in the completed M&A transactions. Revenue from equity underwriting significantly increased on a yearon- year basis, reflecting high revenues from IPOs and follow-ons. Fixed income underwriting revenues increased on a year-on-year basis, primarily driven by high bond issuances. Morgan Stanley’s global reach supported its ability to lead cross-border transactions, and the bank regained its premier leadership position in equity underwriting league tables as global market volumes ticked up. The bank saw building momentum in IB in its M&A and underwriting pipelines across corporate and financial sponsor clients.

Bank of America’s IB fees increased by 35% YoY in Q1’24 with revenue from the advisory, debt underwriting, and equity businesses increasing by 3%, 37%, and 116% YoY, respectively, in Q1’24. The bank’s results reflect the benefits of investments made in its middle market IB and dual coverage teams.

Citi’s IB revenues increased by 32% YoY in Q1’24, driven by debt capital and equity capital markets, as improved market sentiment increased issuance activity. The upside in revenues was partially offset by low advisory revenues, driven by the impact of low merger activity announced in 2023. The bank is cautiously optimistic that it could see a measured reopening of the IPO market in Q2’24, due to improved market valuations.

Deutsche Bank’s revenue from origination and advisory (O&A) business increased by 54% YoY in Q1’24, the highest level since the last nine quarters. The upside in revenue was driven by a 67% YoY increase in debt origination revenues, reflecting a recovery in the leveraged debt market and robust investment-grade issuance. This growth also reflected improved market activity and market share gains. The bank’s share of global O&A improved by ~70 basis points over the year 2023 to 2.6% in Q1’24. O&A revenues are expected to be high in 2024, driven by the continuation of the industry’s recovery seen in Q1’24, along with the incremental impact of investments across the platforms. In debt origination, leveraged debt capital markets are expected to build on their strong start of the year, as market conditions remain favorable for issuance, and an increase in M&A activity is expected to further drive demand for financing.

Barclays’ IB fee income was up by 2% YoY in Q1’24, due to the increased fee income in debt and equity capital markets, which were more than offset by low fee income in advisory and low income in transaction banking. Fees in equity and debt capital markets increased by 36% and 18%, respectively, reflecting improved fee pool and market share, with advisory income decreasing 30% against the same period in 2023. Bank’ IB business delivered a RoTE of 12.0%, reflecting the benefits of diversified income streams, with an increase in equities and IB fee incomes offset by a decrease in FICC income due to low client activity and costs and a net credit impairment release, following improvements in macro-economic outlook.

UBS’s global banking revenues increased by 127% YoY in Q1’24, mainly due to the consolidation of Credit Suisse revenues and other PPA effects. The bank’s revenue from advisory services increased by 11% YoY in Q1’24, mainly due to higher merger and acquisition transaction revenues. Capital market revenues increased by 220% YoY in Q1’24, mainly due to USD 288m of the aforementioned PPA effects. Excluding these effects, underlying capital markets revenues increased by 85%, with increases across all products. Revenues of leveraged and debt capital markets increased by 245% and 58% YoY, respectively, in Q1’24, whereas equity capital markets revenue increased by 58% reserved. evalueserve.com Sources: Refinitiv, press releases www.evalueserve.com Sensitivity: Public during the same period. The bank carried positive momentum in global banking as it outperformed fee pools across all regions, most notably in the US, where banking now contributes a third of total IB revenues, up from less than 20% a year ago.

Advisory firms struggled under challenging market conditions

Similar to Investment Banks, major advisory firms witnessed a revival in revenues in Q1’24. Most advisory firms acknowledged increased risks associated with the current geopolitical, economic, inflationary, and market conditions. However, they see improvements in the availability of debt capital and are optimistic about deal making for remainder of 2024.

M&A advisory firms – Performance highlights

Evercore’s advisory fees decreased by 7% YoY in Q1’24, reflecting a decline in revenue earned from large transactions during Q1’24. The firm has advised companies on some of the most notable transactions that have been announced year to date, including General Electric on its spin-off of GE Vernova for USD 37 billion; Synopsys on a USD 35 billion acquisition of Ansys. European advisory team witnessed a slower start to the year, and deal-closing timelines remain elongated compared with 2023. Private capital advisory and fundraising groups had an active start, and the pipeline continues to grow. While the fundraising environment faced some headwinds industry-wide, the firm’s business performed well.

Lazard’s financial advisory revenues increased by 63% YoY in Q1’24. During Q1’24, the bank was engaged in significant and complex M&A transactions globally. The firm’s preeminent restructuring and liability management practices have been engaged in a broad range of complex restructuring and debt advisory assignments. The firm’s record revenue in Q1 reflects an improving M&A environment and reinforces its outlook for a productive year ahead as it continues to make strides in executing long-term strategic plans.

Moelis’ revenue increased by 16% YoY in Q1’24, driven by an increase in fees earned from its non-M&A businesses, compared with Q1’23. The firm continued to execute its organic growth strategy. During Q1’24, it hired three managing directors in the energy sector and one to cover credit funds. Following its strategic investments in core growth areas, the firm’s pipeline continues to strengthen, and it is better positioned than ever to service its clients as the M&A market recovers.

PJT’s revenue from advisory services surged by 72% YoY in Q1’24. The upside in advisory revenues was due to significant increases in restructuring, strategic advisory and private capital solutions revenues. A core element of that progress is the continued addition of highly talented professionals, with particular emphasis on filling out its strategic advisory footprint. The highest priority for the firm’s strategic advisory business is to ensure that it is best positioned to capitalize on the multiyear M&A upturn that is ahead of it.

PWP’s reported revenues decreased by 22% YoY in Q1’24, mainly because financing and capital solutions were relatively flat year-over-year, while mergers and acquisition revenues were down, primarily due to elongated transaction closing timelines in the current period. While base rates are higher, spreads have narrowed and corporate and sponsor clients have plenty of access to capital. It is financing terms and valuations that present hurdles to transactions, not credit availability. Recruiting remains a strategic priority in its mission to scale the firm. The firm is executing its growth strategy and enhancing its franchise globally with the addition of exceptional talent and world-class clients.

Houlihan Lokey’s financial and valuation advisory revenues increased by 13% YoY in Q4’24, primarily due to an increase in the number of fee events driven by improvements in the M&A markets, which affected one or more of the service lines in the FVA business. The firm entered FY’25 with good momentum in its business and a talented workforce while being realistic about the pace of recovery in this sluggish M&A environment.

The road ahead

Revival in demand for advisory services

The momentum within the underwriting and advisory businesses is expected to continue in 2024, albeit at a slow and varying pace. The momentum will be driven by strong market sentiments, low volatility, and more attractive valuations. The persistently elevated debt costs are expected to further drive demand for IPOs and other equity issuances. Much of the recovery in 2024 will be triggered by a combination of refinancing, sustainability-led initiatives, and event-driven acquisitions. Therefore, revenue from issuances and advisory is expected to outpace that of the trading division. Sable monetary policies and low market volatility in many regions should compress trading revenue growth. Nevertheless, IB revenues may not reach the highs of 2021 in the near term.

Rise of activist campaigns

Following a brief decline during the pandemic, shareholder activism rebounded to pre-pandemic levels in 2022 and continued in 2023, despite macro headwinds and a challenging execution environment. While small and mid-cap companies continue to constitute the majority of activist targets, large-cap companies now represent 30–35% of campaigns, compared with 20% two years ago, with Europe leading the change in mix. Improvements in operations and even outright calls for management team changes have taken center stage, which is a deviation from traditional activist campaigns. Heading into 2024, current elevated levels of activism campaigns, especially directed at large-cap corporates, are expected to continue.

Resilience of the older economy sectors

Following the post-COVID-19 growth cycle, there has been a meaningful sector shift towards capital market activity in older economy sectors such as industrials, materials, power, and natural resources. In reserved. evalueserve.com Sources: Refinitiv, press releases www.evalueserve.com Sensitivity: Public particular, natural resource companies were active across all verticals, representing a quarter of total volumes, including the two largest transactions of FY’23. More broadly, focus on the future of energy and natural resources has led to reevaluation and refocusing of portfolios through divestitures and structured separations, as well as investment through CapEx and M&A in transition and technology. Over the next decade, the growth is expected to be led by renewable energy investment in the sector.

Financial sponsors M&A to gain prominence

FY’23 witnessed a slowdown in sponsoring M&A due to increasing borrowing costs, macro and operational risks, and the growth of the secondary market, which created the largest vacuum for improved sentiment next year. As global M&A volumes stabilize and the institutional leveraged loan market becomes increasingly supportive of M&A financing, the environment is primed for sponsor activity to gain steam. Financial sponsors will likely remain both active as buyers and sellers in the backdrop of record levels of dry powder and being forced to return capital to investors, which was the lowest in the last four years.

Trends for corporate separation to continue

Corporate separation activity, with companies spinning off parts to streamline their businesses, was resilient in 2023 despite capital market volatility and will continue so in 2024. Currently, two-thirds of the S&P 500 companies have three or more large segments, with revenues of >$500 million. These segments are driven in part by a decade of merger activity and portfolio diversification born from a bigger is better philosophy, following the global financial crisis. This led to companies being more complex and provide ample opportunities for spin-offs and carve-out activities to thrive. High levels of spin-off activities in the recent past and positive investor reactions to them will likely drive activity in the space going forward.

Cross-border M&A driven by regional economic issues

Given Europe’s geographic proximity to geopolitical conflict areas of Russia-Ukraine and Israel-Hamas, economies in the region have underperformed compared with the US and emerging economies, which, in turn, has driven European companies’ interest in increasing their exposure to alternate markets. Other potential cross-border M&A may include Japanese companies seeking to invest capital and increase yields outside of the country, as it continues to emerge from deflation.

Generative AI deals to gain pace

Following some periodic adjustments in investment pace, the overall trajectory for AI investment remains robust in Q1’24 and the period witnessed tech giants spending unprecedented sums of money to invest in artificial intelligence startups to avoid falling behind in the generative AI boom as well as public sector is increasingly getting involved in fostering and financing AI’s future. With the rise of generative AI, more companies are prioritizing deals that enhance their tech stack and put them at the forefront of the AI revolution.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.