Overview

The North American consumer and retail sector concluded Q3 2023 on a high note, as US retail sales surpassed expectations due to increased spending on motor vehicles, restaurants, and bars. Overall, despite higher prices and borrowing costs in the region, consumer spending was robust across retail channels.

As reported by the University of Michigan, consumer sentiment dipped to 63.8 in October 2023, the lowest since May 2023, from 68.1 in September 2023. Most households in the region expect inflation to continue increasing over the next year due to geopolitical crises across the globe. One-year ahead inflation expectations too increased to 3.8% in October from 3.2% in September.

According to the US Census Bureau's seasonally adjusted data, US retail and food services sales grew by 3.1% Y-o-Y to USD2,099.2 billion in Q3 2023, compared with USD2,035.5 billion in Q3 2022. The upside was primarily driven by growth in health and personal care stores (7.9%), motor vehicle and parts dealers (5.9%), and general merchandise stores (5.3%) segments. In September 2023, US retail and food services sales increased by 0.7% to USD704.9 billion and outperformed expectations on an M-o-M basis.

According to Statistics Canada, retail and food services sales in Canada slipped by 0.1% M-o-M to CAD66.1 billion in August 2023 due to a weak performance by motor vehicle and parts dealers, and food and beverage retailers. The advanced readings suggest that sales remained slow for September month as well.

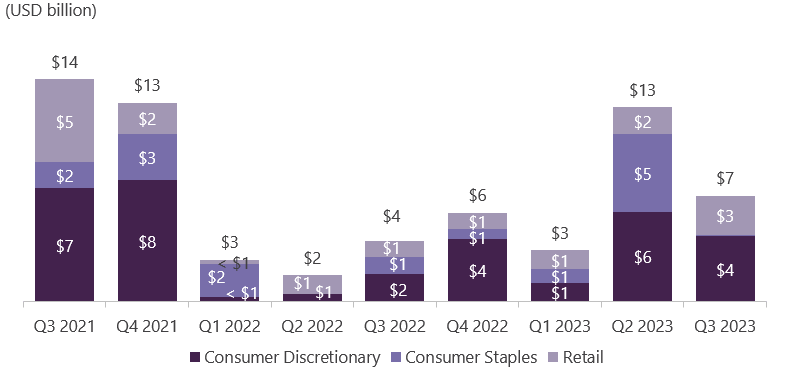

Source: U.S. Census Bureau

According to the US Bureau of Labor Statistics, the unemployment rate in the US stood at 3.9% in October 2023, compared with 3.8% in September 2023. Although the unemployment rate was stable, the number of unemployed people in the US increased by 150,000 to 6.5 million. On the bright side, the retail sector saw the addition of about 7,000 jobs, primarily across motor vehicle and parts dealers; food and beverage retailers; and clothing, clothing accessories, shoe, and jewelry retailers.

M&A Activity

In Q3 2023, the global M&A landscape was rather tepid, with US deal activity accounting for a larger-than-usual share of global activity and compensating for a decline in Europe and Asia Pacific.

The consumer and retail sector in the Americas (North America, the Caribbean, and Latin America) witnessed a robust resurgence in M&A activities, which soared by 93.3% to USD48.9 billion in Q3 2023, up from USD25.3 billion in Q2 2023. The upside was primarily fueled by a significant uptick in M&A deals within the consumer staples and consumer discretionary segments. Notable transactions include JM Smucker's acquisition of Twinkie owner Hostess Brands for USD5.6 billion and Campbell Soup's takeover of rival food manufacturer Sovos Brands for USD2.7 billion.

The financing environment for leveraged buyouts remained challenging as central banks across the region maintained their high interest rates. As a result, private equity firms had to employ innovative solutions such as earn-out structures and contingent value rights (CVRs) to reconcile price differences. For instance, Roark Capital's USD9.6 billion buyout of the sandwich chain Subway had an earn-out structure.

We anticipate that M&A activities in the consumer and retail sector to be subdued until the end of 2023, primarily due to challenges stemming from a struggling global economy.

Source: Refinitiv Deals Intelligence

Bankruptcies

By October 18, 2023, 25 retailers in the US had declared bankruptcy. This number is close to the cumulative number of bankruptcies filed during the same period in 2021 and 2022. Notably, in October 2023, Rite Aid (one of the largest pharmacy chains in the US), JLM Couture (a bridal wear retailer), and DirectBuy Home Improvement (a home improvement product retailer) filed for bankruptcy. The surge in bankruptcies can be attributed to increasing debt loads due to high interest rates and inflation. We expect more retailers to file for bankruptcy protection in the coming months.

Source: S&P Global Press Releases

Due to a change in the Global Industry Classification Standard in March 2023, as well as a methodology change to exclude distributors, results starting with the April 2023 publication will not match prior publications.

Capital Market Activity

The value of debt-raising activities in the Americas slipped by 26.1% to USD30.1 billion in Q3 2023 from USD40.8 billion in Q2 2023. The downside can be attributed to fewer debt-raising activities within the consumer discretionary and consumer staples segments.

The relatively high interest rate environment significantly slowed down both LBOs and the broader M&A market. However, refinancing activities continued to be the primary driver of new deals in the high-yield bond and leveraged loan markets. Leverage loan repricing activity recovered during the quarter, with issuers revisiting prior loans to negotiate lower margins amid improving market conditions.

We expect a resurgence in M&A and LBO activity once the Fed concludes its tightening cycle in 2024. We also expect market conditions to gradually improve and provide borrowers and lenders with increased relief.

Source: Refinitiv Deals Intelligence

The value of equity-raising activities in the Americas declined by 45.6% to USD6.8 billion in Q3 2023 from USD12.5 billion in Q2 2023. The downside was primarily driven by a significant drop in equity-raising activities within the consumer staples and consumer discretionary segments. The slowdown in IPO activities can be attributed to factors such as high inflation, rising interest rates, and an uncertain economic scenario.

We anticipate a potential increase in IPOs in early 2024, if returns remain favorable and market conditions continue to ease.

Source: Refinitiv Deals Intelligence

The Road Ahead

Consumer spending is a crucial driver of economic growth, but the current high borrowing costs and inflation pose challenges to consumers, particularly those that rely on debt for purchases. The US central bank's effort to address inflation by increasing interest rates has led to an 11-year high in credit card delinquencies.

In Q4 2023, we expect the US economy to slow down due to a weak job market and consumer spending. The Federal Reserve's tightening monetary policy, higher bond yields, stricter lending standards, and the strain of a persistently high inflation rate are anticipated to exert a moderating influence on the economy towards the end of 2024.

Geopolitical events, such as the Israel-Hamas conflict in the Middle East, can potentially raise energy prices. Therefore, consumers, especially those that are sensitive to changes in gas prices, will likely reduce their spending as higher gas prices will impact their budgets.

In the debt market, issuance remains concentrated in higher-rated credits, with a preference for secured borrowing. The resurgence of IPO activity hinges on the performance of prominent IPOs in the medium term. We expect a solid IPO pipeline in the late first and second quarters of 2024, contingent on the stability in interest rates and economic conditions, as well as companies' willingness to accept valuations as per pre-pandemic norms.

The venture capital (VC) market is anticipated to continue its gradual recovery, with VC firms increasingly seeking proven business and product-market fit and requiring more investor-friendly provisions.

Looking ahead, the North American consumer and retail sector is expected to navigate a dynamic landscape influenced by a range of factors, from economic indicators and market activities to geopolitical events. As we anticipate shifts in employment, spending patterns, and market dynamics, the road ahead remains both promising and challenging. It is important for companies in the sector to be abreast of what is happening in the employment and debt markets, as well as understand the repercussions of global geopolitical crises on their businesses and consumer sentiment. We believe the stage is set for a period of careful navigation and strategic decision-making, with opportunities and challenges shaping the trajectory of the consumer and retail sector in the coming months.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.